Why Intel breaking a new high post 1H26 results and guidance?

投資人到底看到了什麼而加碼Intel讓盤後暴漲創高?

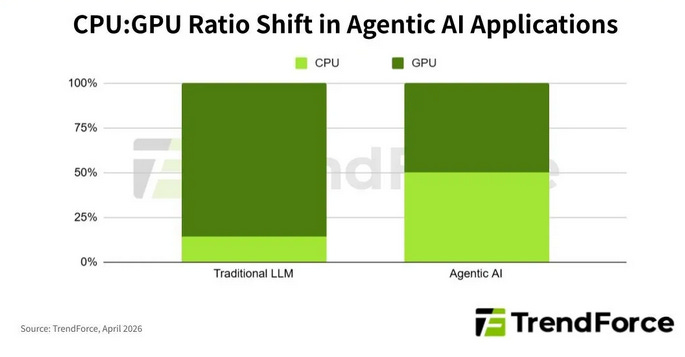

即使英特爾第一季又認列了一筆一次性的龐大40億美元改結構虧損,但上半年營收,毛利率都明顯優於預期,尤其是被Agentic AI 帶動的數據中心CPU需求復甦,A18 良率逐步改善,14A及先進封測進展順利,價格調整,代工跟數據中心的營業利潤率改善,二季度將轉虧為盈,加上以後對Tesla 將收取14A授權金,資本開支可控的狀態下,這些正面訊息應該是讓盤後股價創高暴漲的原因。

1Q26 sales beat market by 9%: Driven largely by stronger than expected data center and foundry sales, Intel reports 1Q26 sales of US$13.577bn, -1% qoq and 7% yoy but 9% above Bloomberg estimates;

Source: Bloomberg 2Q26 guided sales also better than market by 9%: Intel guides 2Q26 sales of US$13.8-14.8bn, up moderated 2%-9% qoq but also 9% above Bloomberg estimates;